Building Pin Payments and the Hidden Cost of Taking On Australian Banks

Grant Bissett co-founded Pin Payments in 2011 to solve a problem that was holding back the entire Australian startup ecosystem. Payments!

Grant Bissett co-founded Pin Payments with Dom Pym in 2011, eventually exiting to Checkout.com. Pin Payments was started at a time where payments infrastructure was stuck inside legacy systems, making it hard to launch a new business and sell globally from Australia.

In this story we dive into:

Competing against Braintree and Stripe

The shit-show of legacy tech that is the Australian banking system

How the Australian banks impacted the value of Pin Payments

Transitioning out of the CEO role

The Problem That Had to Be Solved

Scott Handsaker: What was Pin Payments as a business?

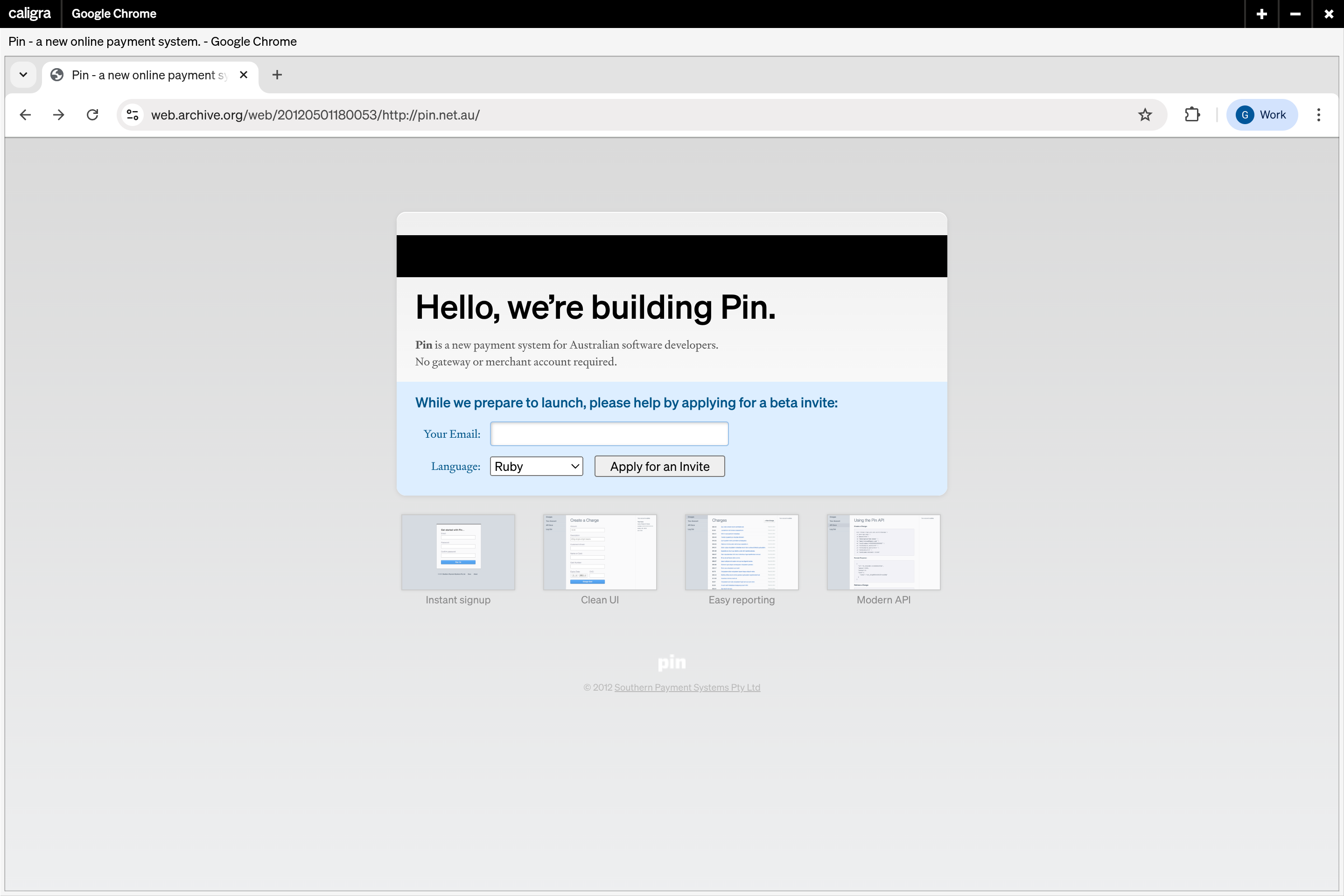

Grant Bissett: Pin Payments was an e-commerce payment facilitator. But really, it was an attempt to update Australia’s internet payments capabilities.

We started the company at the end of 2011. The team had a lot of software experience with our own products, client projects, and companies. Every time we were building something online, there would be this payment problem. Australia didn’t really have products like Stripe and Square. We couldn’t build from Australia.

Every time we got to the point of taking people’s money, it was broken. We thought it’s kind of inevitable that that gets fixed, but can we participate in that change? We wanted to work and live in Australia and build projects, build companies, build products. But we couldn’t do it if we couldn’t participate in the commercial internet without these payment capabilities.

The Stripe Question

SH: Stripe was around when you started. What about Braintree? Did you see them as competition?

GB: We thought about them as really inspiring. We loved their products. Braintree was a little bit ahead of Stripe, established a bit earlier with a slightly different approach. We’d been watching both of them. It seemed like the obvious solution to the problem. Use everything we know about the internet and do that for money.

We loved them from a product point of view, but that didn’t translate into ideas about how to collaborate with them. When we started Pin, Stripe weren’t in the Australian market yet. Braintree came first with a technical solution that went in front of the merchant accounts. The banks don’t provide technology that developers can use, so Braintree was the gateway that made it easier to integrate with financial services.

Later, Stripe entered the market with a more all-in-one solution where you don’t need that banking relationship. You can get it all from Stripe. That’s exactly what we started.

Behind the scenes, there was a lot of concentration. Only one bank in Australia had multi-currency payment capabilities. All of us were building on the same platform, and behind the scenes it’s the same shit show of legacy tech, legacy thinking, no automation, no consistency, no APIs. Just large-scale retail bank infrastructure. Each of us were wrapping that mess up and building a more modern front end.

SH: Was your approach similar to Stripe? My understanding of Stripe’s approach was very developer-first, developer-friendly. Was that the same for Pin?

GB: That was our go-to-market. Imagining the developer as the customer was the most focused, clearest problem we were solving.

We built a product that fixed that, and it taught us about what small businesses need. We discovered this other market of millions of small businesses. Australia had several million businesses with under two million in revenue. They all shared this payment problem, they just described it differently. Whereas a developer might complain about APIs and technical capabilities, we found millions of people saying, “I’m trying to pay my rent, but I can’t take my customers’ money.”

It’s a really urgent, critically important problem solved with the same technology, but just with different language. Our developer audience was the same as Stripe at launch, but then we discovered this broader opportunity around just fixing payments for people. That’s where we diverged. Stripe kept building the best SDK, the best toolkit for doing things with money. Pin over time evolved into something more like Square in terms of its customers. It was very SMB-focused. Our job was just to get you your money from your customer, whether that’s via an API or something else.

Building the Foundation

SH: Were you aiming to build a global company or were you focused on Australia?

GB: Day one, it was just fixing it for Australia with the assumption that we would then expand one by one to different regions. It should have been a global project, as the needs of an e-commerce or SaaS business are fairly portable. If you’re doing anything in a regulated industry, that global rollout is very different to just opening up your website worldwide. So we weren’t sure how to approach that scaling thing. The plan was Australia first, then New Zealand was obvious, then the UK was next.

SH: Who were the founders of Pin?

GB: That’s myself and Dom Pym. Dom and I have worked together for a long time on a variety of projects. Dom’s built so many companies and is a very experienced entrepreneur.

Initially, the idea was I would build the product and Dom would do everything else. In practice, it didn’t really work out that way. In the early days of a startup, everyone does everything.

What Dom brought right at the beginning was a design for a custodial system that managed the funds in the payment system. He had a design he’d already tested and partnerships with financial services firms that could build that. So it was legally proven and technically proven. We had the relationships to implement it, and that was a massive part of what enabled us to get started with Pin.

We weren’t just two guys with a startup idea walking into banks and demanding special facilities. We came in with the support from Perpetual (the oldest financial firm in Australia), and a really well-tested custodial system with novel automation and controls around it.

It started with two of us doing everything, and then over time I was running the business. I was very product and tech-oriented, so that meant I had to bring in others on the operations and commercial side and grow things from there.

The First Signs of Life

SH: When did you first know it might be working? When did you feel that buzz?

GB: There were different stages. The first one was just the pre-launch list of people who wanted this thing. The problem we were solving was just so clear to a lot of people. The value proposition was crystal clear. They really needed it.

When startups talk about finding product-market fit, we kind of skipped that step because we were solving something that seemed so obvious to a particular audience. That was super encouraging. It was proven from the start that there was a list of people who wanted this thing, and they were ready to buy as soon as we could get the product to them.

The first time we technically thought it would work is when we built it for ourselves. We didn’t have the bank’s permission. We just built it. But when we had to think about building a company around it and offering it externally. We knew it would work when we saw those pre-launch signups.

SH: Do you remember who the first customer was?

GB: I remember the first transaction was an e-commerce website selling clothes. There was one sale for a skirt or a t-shirt, and we earned maybe 50 cents. That was a huge milestone.

The True Challenge: Australian Banks

SH: I would think of launching a payments business as being harder than a standard SaaS business. You’re dealing with regulation, concerns of money, legacy software. What were some of the biggest challenges?

GB: There are challenges that we know about that make it difficult. A highly regulated industry, aggressively competitive, and just the importance of the subject matter. If you lose someone’s money, that’s a problem. If their website’s down, it’s a different type of problem. We know it’s going to be hard.

But the challenges that surprised us were when we learned about what happens when you have a regulated activity that interacts with a very established, highly concentrated network of people that you need to work with. The dynamics of the industry behind the scenes was more challenging than we anticipated. And I think it actually has consequences that are really significant for Australia’s startup and innovation scene in general.

Australia’s banking industry is highly concentrated and it’s an impediment to innovation. I think it gets in the way. It slows down innovation and progress in commercial development. That really surprised us.

SH: Do you have any particular stories around that?

GB: The obvious ones are technical. Everyone can relate to a large bank or telco having technology that doesn’t really match consumer expectations. Maybe your bank goes offline for a weekend for maintenance. There were technical challenges where the systems weren’t available when we needed them, or the systems don’t behave in consistent ways.

When your system is misbehaving and the stuff it represents is people’s money, that escalates quickly. If you send me back the wrong number and the wrong amount goes into an account, that’s a problem.

I had a relationship with a banking provider. Another startup, say Stripe or Braintree, might have a relationship with that same provider. What if that bank actually sends my customers’ money to Stripe or Braintree? That sort of thing happened more than once. These are just incompetent mistakes that happen.

But it gets worse. These are technical faults, but then there’s the more strategic, more challenging stuff where the banks could interfere with the development of a startup.

A bank once blocked our funding when the company really needed to get more capital into the business. They have ways of doing that by talking about seniority of debt and that sort of thing. They interfered with an M&A transaction and blocked that. They forced us to enter into agreements and then changed the terms shortly after.

I would say Australia’s banking industry decimated the value of our startup. That is not an exaggeration. And I don’t have any reason to expect that they’re not doing that across the board. I think it’s a real impediment to innovation and growth in Australia.

SH: Were they acting economically rationally or were they bad corporate citizens?

GB: I’ve definitely had times where I felt they’re acting in bad faith. But the challenge is it’s not the institution that’s operating that way. It’s one team, one individual, or one division.

You can have these situations where everyone is acting quite rationally, but the sum of those actions is pretty hostile and in bad faith. There’s this saying about never assuming malice when something can be explained by incompetence. If we’re talking about large Australian retail banks, I think you can assume both. I started to think of them as like a drunk baby with a machine gun. Lots of incompetence, lots of carelessness, and a readiness to take some really destructive actions.

SH: Would you build another payments business in Australia? Or does the environment turn you off?

GB: I’m quite happy to be working outside of fintech currently, but I think there’s just so much opportunity. We haven’t even begun to bring that industry online yet.

There are significant benefits to improving those systems. I don’t care about banking or fintech or credit cards or any of that stuff. No one cares about the mechanics. We care about the consequences. And when you’re talking about money, this is social mobility and accessibility and all of this good stuff. There’s an abundance of meaning that’s still trapped behind this shitty, concentrated, old-school industry. So yeah, I would absolutely go back into payments one day.

The CEO Journey

SH: Your role sounds like you were originally going to be very product and technology focused, but it turned out you were actually the CEO for a number of years. How did you enjoy that role?

GB: I like learning and I like making things. I think the startup journey is just massively educational. It’s very introspective, very educational, very challenging. All that stuff which I really like.

What I didn’t like so much is not knowing the level and the consistency of the challenge. It’s hard. We all know that startups are hard. But they’re hard in terms of relationships and psychology and mental health and your wellbeing and all of that stuff. That was challenging.

A long time ago, I thought maybe there were gaps and areas where I should be improving, be more rounded, be more capable in different areas. I’ve given up on that. That’s bullshit. I know who I am. I know what I’m good at. It’s actually more effective to hire the folks who are experts in the areas where I’m not so proficient.

Understanding the Business

SH: Do you recall your standard revenue metrics as you grew?

GB: I don’t know when we got to the first million in revenue, but I do remember when we had the first understanding of the seasonality of the business. That was a really weird thing to go through.

We ran an e-commerce platform and everyone knows that holiday season is a big deal for these kinds of businesses. Meanwhile, Pin was serving all these small businesses, and a lot of them were organizations that had membership fees or something other than an e-commerce retail purchase. Because of the composition of our customer base, we had a massive spike in March.

Things would decline, and then we would see the same again next year. That went on for a decade! It was just something counterintuitive, something unexpected because of the customer base we had.

That probably coincided with the first million in revenue.

The Fundraising Journey

SH: I know you raised from angels early on. Tell me how you thought about fundraising for this business?

GB: It was all angel-style early on. There was an angel round super early, might have been half a million dollars to get started. Then we brought in a handful of other angel-style investors who were experienced startup folks in Melbourne and Sydney.

That went on with small equity rounds right at the beginning, then convertible notes or safe notes over a period of years. That got us into market and got the business established. We sort of skipped over a seed round and then did a proper Series A with a fund.

It was in 2015 that we raised a Series A round with VIXS Investments, who had a fintech fund in Australia. That was the first time we brought in a VC-style fund into the business.

SH: Did much change when you took on institutional capital?

GB: It changed our network a bit. It didn’t significantly change reporting or operations or targets for the business. It didn’t change much about what we were doing. That’s why they were the right investor, as they were looking for what we were doing in our area.

SH: Blackbird, Square Peg and AirTree would have existed. Did you talk to them at all?

GB: I’m sure we spoke to everyone, including those three. I’m sure with Pin we spoke to probably 20 more names you would recognize.

One challenge we had was that when we started, VC in Australia was just getting started. Blackbird was just beginning, was just very early. It was a different scene to what it is today. By the time we’re a few years in market and understood the dynamics and growth of the business, there was a point where we had a healthy, happy business that was growing every year, but maybe it wasn’t on trend with the thematics of VC or it didn’t have the growth characteristics that matched what the VCs were filtering for at the time.

We struggled with that a lot. If we were a little bit more on trend, I think some of those discussions might have been easier.

The Leadership Transition

SH: I know you stepped away from being CEO. Talk me through the thinking at that point.

GB: It got to a point where it was clear that this was a business that, going forward, is better served as a sales organisation more than an R&D organisation. It’s more of a scaling phase than a design phase.

Meanwhile, I’d been working with Chris Dahl at Pin who we brought in really early on to build the commercial business. Chris built the sales motions, the distribution systems and networks. Chris had been building that for years. And Caitlin Zotti had been working as the COO, managing all the operations. It seemed like it was the right time because what served the business best was what those two were doing best. So Chris and Caitlin both stepped into the role of Co-CEO.

It no longer made sense to treat it like the early stages of the startup where you’re defining what the thing is. It’s more about operating and scaling. So that was the right time.

SH: Was it a hard decision for you to make?

GB: It was an easy decision aside from timing. It was easy for me to understand that it would happen at some point. But the hard part was when do you know it’s the right time?

It got to a point where it’s abundantly clear that this is the next stage for this business. If I were to lead it, I would recruit expertise to execute. And I’ve got those people right next to me. May as well hand it over to them.

The Exit

SH: You ended up exiting to Checkout.com. Was that a merger or an acquisition?

GB: It was an acquisition. Pin sold to Checkout.

SH: Prior to that happening, you mentioned you got one M&A blocked by one of the banks. Did you have any other interest from parties?

GB: We had a couple of transactions that didn’t proceed in a variety of ways. We had some people who were interested in acquiring this kind of business because perhaps they already had a similar business and were just expanding it, or perhaps they had similar relationships with the financial services backends but didn’t have a distribution channel.

Others were more like a SaaS business looking to expand its revenue by incorporating payments. We had several different scenarios that we contemplated, and several different deals that commenced that didn’t conclude for a variety of reasons.

With Checkout, that was related to a process that we ran with an advisory firm in Melbourne called Platform Partners. We could either put together a Series B story and fund it and expand ourselves, or we could put this into an organisation that has the security and financial services capabilities that we need to build on top of.

That was a dual process that we ran quite deliberately. We went out to market looking for what was out there and found a few folks that were interested in buying these kinds of businesses.

It was quite a deliberate process at that stage and probably the first time that fundraising had been so deliberate for the business. Whereas in the early stages it’s sort of raising capital because you need money, this was a much more deliberate process.

The Hardest Question

SH: Was there ever a time during the journey where you thought, “We’re not going to make it”?

GB: There was the routine startup stuff where your runway is getting really short, and you’re running out of cash. Then it’s difficult to find new investors or find new ways to fund the business or new ways to cut costs. That happened a lot and that was really stressful, but quite generic in a way. Every startup has that.

So that was stressful but pretty standard. There were times where we weren’t sure how we were going to get through those times, but there were never times where we were in doubt about the opportunity around what we were building. Pin was always growing from the start. We knew the size of the problem that we were working on and we saw that the business was growing and we believed in it.

The Wrapup Questions

SH: What is a book we should all read?

GB: I Am a Strange Loop by Douglas Hofstadter. It’s a contemplation on where consciousness comes from. While everyone’s talking about artificial intelligence, this is not that. This is a question about what intelligence is, what consciousness is, but it’s an easy way to read about that kind of subject matter without any particular belief framework associated with it. A fun bit of philosophy.

SH: What is a podcast we should all listen to?

GB: I don’t listen to podcasts. I can’t recommend a single one. I just don’t know.

SH: Either do I. I thought I was the only person in the world. I probably listen to about one every two months when there’s a guest I just want to listen to, but typically I don’t. I read books. That’s where I get my information.

GB: Three hours of talking. Who wants that?

SH: Yeah not me. Okay, what is a band or artist we should all listen to?

GB: Everyone should listen to Éliane Radigue while we can. She is a French composer and artist making really fine, let’s call it drone sound art, that needs a lot of attention and contemplation. It really rewards some attention and some time. She’s in her 90s now and still practising and still giving interviews.

This is an amazing person making really fine work that reminds us of what we can get from slowing down and giving things some attention. The total opposite to a podcast, the total opposite to some cynical pop music stuff. It’s actually like, what do you do when it’s time to stop and think? I like to be reminded of that.

SH: Thanks for your time Grant!